The Project Gutenberg EBook of Weather Crops and Markets, by Anonymous

This eBook is for the use of anyone anywhere in the United States and

most other parts of the world at no cost and with almost no restrictions

whatsoever. You may copy it, give it away or re-use it under the terms

of the Project Gutenberg License included with this eBook or online at

www.gutenberg.org. If you are not located in the United States, you'll

have to check the laws of the country where you are located before using

this ebook.

Title: Weather Crops and Markets

Vol. 2, No. 6

Author: Anonymous

Release Date: April 25, 2019 [EBook #59362]

Language: English

Character set encoding: UTF-8

*** START OF THIS PROJECT GUTENBERG EBOOK WEATHER CROPS AND MARKETS ***

Produced by Richard Tonsing and the Online Distributed

Proofreading Team at http://www.pgdp.net (This file was

produced from images generously made available by The

Internet Archive)

Transcriber’s Note:

The cover image was created by the transcriber and is placed in the public domain.

105

WEATHER

CROPS AND MARKETS

Published Weekly by the

United States Department of Agriculture

CERTIFICATE: By direction of the Secretary of Agriculture the matter contained herein is published as statistical information and is required for the proper transaction

of the public business. Free distribution is limited to copies “necessary in the transaction of public business required by law.” Subscription price $1 per year

(foreign rate $2) payable in cash or money order to the Superintendent of Documents, Government Printing Office, Washington, D. C.

| Washington, D. C. |

AUGUST 5, 1922. |

Vol. 2, No. 6 |

EXPORT BUTTER DEMAND CAUSES MUCH INTEREST

Sales to United Kingdom Strengthened Early Summer Market—Shift in England’s Supply Sources.

A demand for American butter by English

buyers had a materially strengthening effect

on the early summer market in the United

States. This generally unexpected export

demand has called forth various explanations

in the attempt to determine the probability

of continued demand from that

source.

An analysis of the international butter

trade of the past 10 years indicates that a

change not yet generally realized has taken

place in the seasonal trend of imports of

butter into the United Kingdom, which

largely accounts for this demand in anticipation

of an autumn shortage. This change is

due to the shift that took place during the

war in the sources of supply of that greatest

of all butter-importing countries.

SUPPLY WAS UNIFORM.

Prior to the war the United Kingdom obtained

its butter supply from such widely

scattered sources in both the Northern and the

Southern Hemispheres that the supply was

remarkably uniform from month to month

throughout the year. During the war, when

supplies available from continental Europe

and Russia were reduced, Australia, New

Zealand, and Argentina were encouraged to

expand their dairy industry, and have

together since that time continued as the

most important sources of supply of butter

on the British markets.

As the flush of production in Australia,

New Zealand, and Argentina occurs during

the fall and winter months when production

is lightest in North America and Europe,

England now receives an average of two-thirds

of the total supply of foreign butter

during the winter and spring, whereas formerly

but one-half was received during this

period.

Although consumption does not necessarily

follow the same seasonal trend as the

imports, it is a fact, according to reports of

London dealers, that butter stocks are now

lower than at the same time last year, when

at least 50,000,000 lbs. of Government stocks

still remained unsold in England. With

comparatively light stocks and the certainty

that imports into England after July can

not be as heavy as during the first six months,

a speculative demand has been stimulated

in that country in anticipation of an expected

autumn shortage.

Although butter production since the war

has recovered rapidly in practically all of

the important dairy countries, Russia is still

out of the world’s market. The cutting off

of the Russian exports to England, which

amounted to 150,000,000 lbs. annually from

1909 to 1913, was the greatest single factor

in bringing about, this change in the seasonal

supply of the latter country.

The present statistical position of the

United States is, therefore, somewhat misleading,

unless due consideration is given to

(Concluded on page 111, column 2.)

IN THIS ISSUE.

|

|

Page. |

| Crop Reports |

106 |

| |

Condition of cotton crop on July 25. Truck crop reports. |

|

| |

|

|

| Live Stock and Meats |

107 |

| |

Nearly all classes sold at lower levels. Fresh meat markets were slow. |

|

| |

|

|

| Dairy and Poultry |

110 |

| |

Butter markets weakened under heavy supplies. Cheese prices were lower. Monthly report on condensed and evaporated, and powdered milk markets. |

|

| |

|

|

| Fruits and Vegetables |

112 |

| |

Shipments continued liberal. White potato prices slumped. Most other lines steady to firm. |

|

| |

|

|

| Grain |

114 |

| |

Wheat prices continued downward trend. Cash corn fairly steady. |

|

| |

|

|

| Hay and Feed |

115 |

| |

Hay demand was dull. Feed prices were easier for most kinds. |

|

| |

|

|

| Seeds |

116 |

| |

Reports on Kentucky bluegrass, orchard grass, and meadow fescue seed crops. |

|

| |

|

|

| Cotton |

117 |

| |

Prices declined slightly. Weather reports a factor. |

|

| |

|

|

| Weather |

118 |

| |

Weather favored growth of most crops. |

|

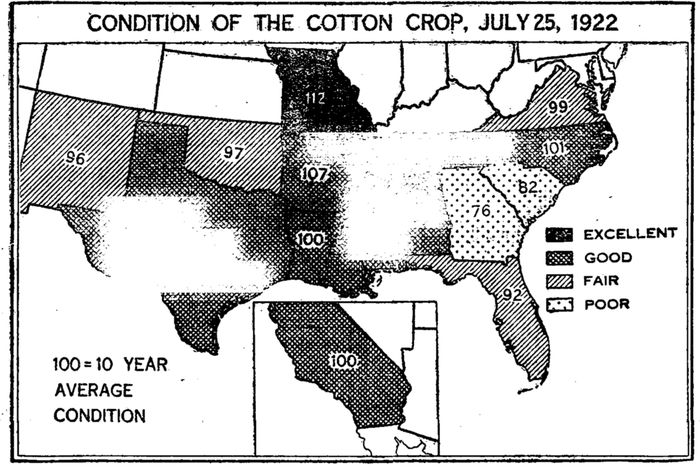

COTTON CROP CONDITION 70.8 PER CENT NORMAL

Loss Amounts to 0.4 Per Cent During Past Months—Total Output Estimated at 11,449,000 Bales.

The condition of the cotton crop on July

25 was 70.8% of normal, according to the

estimate made by the U. S. Department of

Agriculture on Aug. 1. Compared with the

condition of 71.2% on June 25, this shows a

decrease in condition of 0.4% for the month.

The average condition of the cotton crop on

July 25 for the past 10 years stands at 73% of

normal.

A condition of 70.8% of normal on July 25

this year forecasts a yield per acre of about

157.2 lbs. and a total production of about

11,449,000 bales of 500 lbs. gross weight

each. The final outturn may be larger or

smaller than this amount, of course, depending

upon whether or not the conditions that

develop during the remainder of the season

prove more or less favorable to the crop than

such conditions ordinarily prove.

| Condition of the Cotton Crop on July 25, with Comparisons. |

|---|

| |

| [100 = normal.] |

|---|

| |

| State. |

July 25. |

June 25, 1922. |

July 25, 1922. |

Change, June 25 to July 25. |

| 10‒yr. av. |

1920 |

1921 |

10 yr. av. |

1922 |

| Virginia |

81 |

74 |

82 |

85 |

80 |

0 |

‒5 |

| North Carolina |

77 |

77 |

75 |

76 |

78 |

‒1 |

+2 |

| South Carolina |

73 |

77 |

62 |

60 |

60 |

‒2 |

0 |

| Georgia |

71 |

68 |

59 |

58 |

54 |

‒3 |

‒4 |

| |

|

|

|

|

|

|

|

| Florida |

71 |

64 |

60 |

75 |

65 |

‒5 |

‒10 |

| Alabama |

69 |

67 |

58 |

68 |

70 |

‒5 |

+2 |

| Mississippi |

72 |

71 |

68 |

76 |

74 |

‒4 |

‒2 |

| Louisiana |

70 |

71 |

59 |

69 |

70 |

‒7 |

+1 |

| |

|

|

|

|

|

|

|

| Texas |

72 |

74 |

62 |

72 |

72 |

‒6 |

0 |

| Arkansas |

76 |

78 |

76 |

80 |

81 |

‒3 |

+1 |

| Tennessee |

78 |

76 |

75 |

83 |

85 |

0 |

+2 |

| Missouri |

80 |

81 |

80 |

92 |

90 |

0 |

‒2 |

| |

|

|

|

|

|

|

|

| Oklahoma |

77 |

85 |

68 |

76 |

75 |

‒2 |

‒1 |

| California |

95 |

85 |

83 |

91 |

95 |

+2 |

+4 |

| Arizona |

[1]90 |

85 |

89 |

85 |

86 |

[1]+1 |

+1 |

| New Mexico |

|

85 |

88 |

85 |

85 |

|

0 |

| United States |

73.0 |

74.1 |

64.7 |

71.2 |

70.8 |

‒3.9 |

‒0.4 |

Last year the production was 7,953,641

bales, two years ago 13,439,603 bales, three

106years ago 11,420,763 bales, four years ago

12,040,532 bales, and five years ago 11,302,375

bales.

The 1922 acreage of Egyptian type cotton

is estimated at 80,000 acres in Arizona and

less than 1,000 acres in California. In 1921

Arizona had 75,000 acres and California

9,000 acres, while in 1920 the estimate for

Arizona was 200,000 acres and for California

45,000 acres.

The department’s estimate of cotton acreage

in cultivation on June 25, which was

made public on July 3, remains unchanged

at 34,852,000 acres because the acreage

abandoned before that date was excluded.

A great decrease in cotton acreage followed

the high acreage of 1920, which was 37,043,000

acres, because of the disastrous break

in prices to growers in that year.

The accompanying table gives detailed

information on the condition of the cotton

crop on July 25, by States, together with

comparisons.

Paradox in Forecast Yield of Crop per Acre as Indicated by Condition.

A crop may deteriorate in condition during

a growing month and yet its yield per acre

as forecast by a computation based on the

lowered condition may increase. In the

average of crop experiences during the growing

period a certain crop declines in condition

during a certain month by a certain

percentage of a normal condition.

For instance, the cotton crop has a record

of a deterioration of 3.9% of a normal condition

from June 25 to July 25 in the average

of the last 10 years. As a matter of fact,

however, during this period in 1922 the

deterioration in the condition of the cotton

crop was only 0.4%. This is clearly a

relative improvement because it is less than

the usual deterioration of 3.9%. Hence the

yield per acre in the forecast for July 25

must be greater than in the forecast made a

month earlier, notwithstanding the absolute

decline in condition.

Apple-tree tent caterpillars are very numerous

in New England and New York this

year. Farther south these pests are noticeably

less numerous than usual.

Report on Cabbage, Celery, and Onions in Michigan.

Reports from the field service of the U. S.

Department of Agriculture for the date of

July 25 concerning commercial cabbage,

celery, and onions in Michigan contain the

following information:

Cabbage.—Five counties in southern Michigan

have about 1,285 acres of commercial

cabbage compared with last year’s area of

590 acres, or an increase of 118%. The

counties and their cabbage areas are: Ingham

160 acres, Eaton 225 acres, Jackson 67

acres, Hillsdale 233 acres, and Branch 600

acres. The principal increases over 1921

are in Hillsdale and Branch Counties. The

crop is generally in excellent condition.

In Hillsdale County, Jonesville has 200

acres, of which 130 acres are under contract;

Mosherville has 13 acres for kraut; and

Litchfield has 20 acres. In Branch County,

Quincy has approximately 250 acres of commercial

cabbage, of which 170 acres are under

contract: and Coldwater has about 350 acres,

with 60% under contract. The kraut plant

in Coldwater will be in operation this year.

Baroda, in Berrien County, has 60 acres of

cabbage and Niles, in the same county, 40

acres for kraut.

In northern Michigan, Saginaw County

has 1,400 acres of commercial cabbage, 300

acres of which are under contract.

Celery.—The combined area of commercial

celery in Lenawee, Cass, Allegan, and Kent

counties is 1,005 acres, an increase of 450

acres over 1921. Lenawee County has 117

acres, Cass 118 acres, Allegan 170 acres, and

Kent 600 acres. The crop is in excellent

condition.

Onions.—Allegan County has about 603

acres of commercial onions, or 88% more

than in 1921. The Gull Swamp section

(Martin, Gull Plain, Shelbyville, Hooper)

has approximately 550 acres. Other acreages

are: Wayland 8 acres, Dorr 25 acres,

Herps 20 acres. The condition of the crop

in Allegan County is above average. Kent

County has an onion acreage about the same

as last year’s.

Florida watermelons were widely distributed

this season. Some shipments went as

far as San Francisco, Portland, Seattle, Vancouver,

B. C., and other Canadian points.

CONDITION OF THE COTTON CROP, JULY 25, 1922

INTERMEDIATE ONION CROP ESTIMATED AT 6,753 CARS

Early and Intermediate Crops Forecast at 13,605 Cars—Acreage Increased in Late States.

The production of commercial onions in

the seven intermediate shipping States is

forecast at 6,753 cars of 500 bus. each, compared

with a production in 1921 of 4,472

cars, according to estimates of the U. S. Department

of Agriculture for July 15. These

intermediate States are: New Jersey, Maryland,

Virginia, Kentucky, Iowa, Texas,

and Washington.

New Jersey leads the intermediate States

with an indicated production of 1.613 cars,

and following in order are Washington with

1,566 cars, Texas with 1,092 cars, Iowa with

1,062 cars, Kentucky with 600 cars, Virginia,

with 560 cars, and Maryland with 260 cars.

The commercial onion crop in the intermediate

and early States combined is forecast

at 13,605 cars, each car of the early crop

containing 530 bus. and of the intermediate

crop 500 bus. In 1921 the harvest of early

and intermediate onions totaled 10,287 cars.

About 38,000 acres have been planted to

late commercial onions, compared with

about 35,000 acres in 1921, according to the

department’s estimates. The condition of

the late commercial onion crop was 83% of

normal on July 15. This condition is about

average.

The accompanying tables give detailed

information, by States, on the early and intermediate

crops and the late crop.

| Acreage and Forecast of Production of Commercial Onions in Intermediate and Early States. |

|---|

| |

| State. |

Acreage. |

Yield per acre. |

Production. |

| Harvested, 1921 |

Planted, 1922 |

Average, 1921 |

Indicated, 1922 |

Harvested, 1921 |

Forecast, 1922 |

|

Acres. |

Acres. |

Bu. |

Bu. |

Cars.[2] |

Cars.[2] |

| Iowa |

1,200 |

1,600 |

202 |

332 |

485 |

1,082 |

| Ky. |

1,000 |

1,000 |

324 |

300 |

648 |

600 |

| Md. |

500 |

500 |

250 |

260 |

250 |

260 |

| N.J. |

2,400 |

2,400 |

239 |

336 |

1,147 |

1,613 |

| Tex. |

1,000 |

1,500 |

275 |

304 |

550 |

1,092 |

| Va. |

800 |

1,000 |

280 |

280 |

448 |

560 |

| Wash. |

1,300 |

1,500 |

363 |

522 |

944 |

1,566 |

| Total intermediate States |

8,200 |

9,500 |

273 |

355 |

4,472 |

6,733 |

| Early States previously reported[3] |

13,500 |

16,000 |

228 |

227 |

5,815 |

6,852 |

| Total, intermediate and early States |

21,700 |

25,500 |

245 |

275 |

10,287 |

13,605 |

| Acreage and Condition of Commercial Onions in Late States. |

|---|

| |

| State. |

Acreage. |

Condition (100=normal). |

| Harvested, 1921. |

Planted, 1922. |

July 1, 7‒yr. av. |

July 1, 1921. |

June 1, 1922. |

July 1, 1922. |

July 15, 1922. |

|

Acres. |

Acres. |

P.ct. |

P.ct. |

P.ct. |

P.ct. |

P.ct. |

| Calif., central dist. |

7,800 |

6,500 |

90 |

89 |

100 |

90 |

95 |

| Colo. |

800 |

1,500 |

80 |

91 |

90 |

88 |

91 |

| Idaho. |

100 |

300 |

89 |

94 |

88 |

94 |

98 |

| Ill. |

1,100 |

1,300 |

89 |

79 |

75 |

82 |

79 |

| Ind. |

3,698 |

1,600 |

78 |

73 |

77 |

73 |

83 |

| Mass. |

4,500 |

4,600 |

83 |

73 |

78 |

79 |

75 |

| Mich. |

1,300 |

1,700 |

79 |

65 |

86 |

89 |

88 |

| Minn. |

1,300 |

1,300 |

88 |

89 |

85 |

95 |

90 |

| N. Y. |

7,300 |

8,300 |

75 |

78 |

86 |

74 |

68 |

| Ohio |

5,100 |

5,800 |

79 |

73 |

98 |

88 |

88 |

| Oreg. |

900 |

900 |

78 |

80 |

100 |

73 |

79 |

| Pa. |

300 |

400 |

81 |

93 |

100 |

95 |

95 |

| Utah |

100 |

100 |

93 |

94 |

96 |

91 |

90 |

| Wis. |

1,000 |

1,000 |

81 |

82 |

96 |

90 |

86 |

| Total |

35,200 |

38,300 |

82 |

80 |

89 |

82 |

83 |

107

Live Stock and Meats

NEARLY ALL CLASSES OF LIVE STOCK SELL AT LOWER LEVELS

Price Ranges on Beef Steers Widen—Heavy Hogs Break Sharply—Sheep Prices Irregular.

Practically all classes of live stock sold

lower during the week ending July 29. In

beef steer trade the general decline was

assisted materially by the heaviest run of

native, western, and Canadian grassers of

the season. Downturns of mostly 25¢ at

Chicago and of 50¢-$l at some Missouri

River markets were apparent on the more

common descriptions. As supplies of western

grassers increased, the supply of long-fed

bullocks decreased and as the latter were

sought by all interests, the widest price

range of the season on beef steers was

created at all markets.

Hog prices fluctuated sharply, closing

Chicago values being 25¢‒50¢ lower on mixed

grades and heavy packers, and 40¢‒55¢ on

good butcher hogs compared with the close

of the previous week. Much of the supply

at Omaha and a good percentage of the run

at Chicago and some other markets consisted

of heavy sows and mixed packing grades,

and these pulled the general average down

to the lowest levels since early in February.

SHEEP TRADE ERRATIC.

Trade in fat sheep and feeding lambs was

erratic, with closing prices highest of the

week but showing an irregular basis compared

with the previous week’s close.

Receipts at 10 large markets for the week

were approximately 199,000 cattle, 502,000

hogs and 195,000 sheep, compared with

215,357 cattle, 452,902 hogs, and 244,517

sheep the previous week, and 166,112 cattle,

398,424 hogs, and 199,137 sheep the corresponding

week last year.

Cattle.—Receipts of grassers from native

territory, range States, and Canada, assumed

the largest proportions of the season. Short-feds

also were numerous, and long-fed matured

beef steers and yearlings correspondingly

scarce. Canadians were unusually

numerous at St. Paul and Chicago for so

early in the season, the July supply at the

former market up to July 27 standing at 5,800

as compared with 988 for the corresponding

period a year ago. The collapse of cattle

values in Canadian provinces was an incentive

for shipping across the border.

Canadians and Dakotas were generally in

poor flesh and turned at $4.75‒$6.50, killers

taking a few at the latter price. Oklahoma

and Texas grass steers invaded Kansas City

and St. Louis in liberal numbers, and sold

largely within a spread of $4.25‒$7, many

quarantine steers, grading as cutters, selling

around $4.25‒$4.75. Kansas pasture cattle

were well represented at Kansas City, and

winter grass steers of good weight and condition

sold there upward to $8.75 or slightly

higher. A few lots of Utah and California

steers arrived at Omaha. Bulk of grass

steers sold there at $6‒$7.25, a large proportion

of the far western steers being in feeder

flesh. One lot of Montana steers showing

breeding quality and good killing flesh

brought $8.75 at that market from a producer.

This lot met good packer competition,

and the relatively high sale price indicated

the plainness of the early run of

grassers in general.

Long-fed matured bullocks, averaging

1,443 lbs. reached $10.80 at Chicago and

best long yearlings topped at $10.50, the

premium of heavy steers over yearlings continuing

in evidence. Sales above $10.25

were comparatively scarce, bulk of beef

steers at Chicago being of quality and flesh

to sell at $8.50‒$10. At that point few bullocks

that had received even a sparse corn

ration on grass sold under $8, but common

native and western grassers cashed well

below that figure.

PRODUCERS IN MARKET.

The influx of westerns augmented the

stocker and feeder supply and producers

took more notice of their pasture and feed

lot needs than recently, insisting, however,

on lower prices except on kinds of high

quality. A spread of $5.50‒$6.50 absorbed

the majority of stockers and light feeders at

Chicago, a few heavy feeders reaching $7.50,

while good feeders commanded $7.25‒$7.75

at Kansas City, most of the desirable

stockers bringing $6.50‒$7 at that market.

Common light stock steers descended to

$4.50 and lower in instances there and at

St. Louis.

She stock offerings were comparatively

scarce, and flesh condition for the most part

was plain to medium. Highly finished

kosher cows maintained $8‒$8.50 levels and

above at Chicago, corn-fed yearling heifers

selling in line with steers of a similar finish.

In-between grades of beef cows and heifers

lacked dependable outlet, generous runs of

low grade grass steers at river markets being

a weakening influence. Bulk of fat cows

and heifers at Chicago brought $5‒$7.25.

Canners displayed strength, few healthy descriptions

selling there below $3.

Bulls closed largely 25¢ lower; desirable

heavy bolognas cashed upward to $4.75‒$4.85

early at Chicago, but descended to around

$4.50, heavy beef bulls sharing the decline.

Reduced arrivals of veal calves at Chicago

somewhat counteracted the effect of slump

conditions in the dressed market and values

advanced 25¢‒50¢, packers taking desirable

vealers at the close at Chicago at $9.50‒$10,

these interests as well as small killers paying

upward to $10.50 for specialties.

Hogs.—Although receipts at Chicago were

moderate, being about the same as in the

preceding week, those at western points

(Concluded on page 109, column 1.)

MODERATE RECEIPTS OF MOST MEATS IN EXCESS OF DEMAND

Prices Generally Lower on Beef, Veal, Lamb, and Mutton—Heavy Pork Loins Also Lower.

(Boston, New York, Philadelphia, and Chicago.)

Moderate receipts of beef, veal, lamb, and

mutton were in excess of the limited demand

and prices were generally lower for the week

ending July 28. Heavy pork loins were

weak to lower with other classes steady to

higher, except at New York, where all

averages shared in the decline.

Beef.—Moderate receipts of beef at eastern

markets found a limited outlet. Good and

choice grades of steers were not plentiful,

but were neglected in favor of poorer grades

as prices were given more consideration than

quality. The demand for chucks and

rattles showed some improvement, and

prices on these were relatively firmer than

on other cuts. Cows were mostly of medium

and common grades and were hard

to move. At Chicago the assortment of

steer beef was good, but prices weakened

under a narrow demand. Few desirable

cows were available, most of the supply

having consisted of the poorer grades.

PRICES UNEVEN AT CLOSE.

Compared with the close of the preceding

week. Boston was about steady, New York

unevenly 50¢-$3 lower, Philadelphia $1‒$2

lower, and Chicago $1 lower. Cows were

weak to $1 lower at Boston, $l-$2 lower at

New York and Philadelphia, and 50¢ lower

at Chicago. Receipts of bulls were light,

and prices closed steady to $1 higher at

Boston, steady to $1 lower at New York,

and 25¢‒50¢ lower at Chicago, with very

few on sale at Philadelphia. Kosher beef

trade was slow, and prices closed around $1

lower at New York and unchanged elsewhere.

Veal.—Except at Boston the demand for

veal at eastern markets was poor after the

early part of the week, and prices declined

daily. At that market western dressed

receipts and local slaughter were light and

demand fair. At Chicago the fairly liberal

offerings were too great for the slow demand,

and the market had a weak undertone.

Compared with the close of the preceding

week, Boston was steady to $1 lower. New

York $2‒$3 lower, Philadelphia $2‒$4 lower,

and Chicago $1 lower.

| DAILY AVERAGE WEIGHT AND COST OF HOGS, WEEK ENDING JULY 29, 1922. |

|---|

| [Price per 100 pounds.] |

|---|

| Market. |

Mon. |

Tues. |

Wed. |

Thurs. |

Fri. |

Sat. |

This wk. |

Last wk. |

1 yr. ago. |

| Wt. |

Cost. |

Wt. |

Cost. |

Wt. |

Cost. |

Wt. |

Cost. |

Wt. |

Cost. |

Wt. |

Cost. |

Wt. |

Cost. |

Wt. |

Cost. |

Wt. |

Cost. |

| Chicago |

259 |

$9.73 |

269 |

$9.52 |

252 |

$9.45 |

267 |

$9.25 |

266 |

$9.24 |

277 |

$9.24 |

263 |

$9.44 |

261 |

$9.53 |

252 |

$10.35 |

| E. St. Louis |

200 |

10.70 |

198 |

10.71 |

218 |

10.36 |

203 |

9.96 |

205 |

10.03 |

199 |

10.22 |

202 |

10.33 |

199 |

10.66 |

201 |

11.33 |

| Kansas City |

212 |

10.24 |

217 |

9.96 |

217 |

9.76 |

219 |

9.49 |

200 |

9.55 |

216 |

9.36 |

217 |

9.85 |

217 |

9.95 |

228 |

10.47 |

| Omaha |

261 |

9.06 |

273 |

8.81 |

280 |

8.46 |

273 |

8.20 |

273 |

8.32 |

281 |

8.43 |

274 |

8.54 |

265 |

9.00 |

265 |

9.54 |

| St. Joseph |

233 |

9.71 |

233 |

9.75 |

233 |

9.50 |

246 |

9.16 |

250 |

9.04 |

234 |

9.32 |

238 |

9.45 |

238 |

9.67 |

|

|

| S. St. Paul |

277 |

8.45 |

282 |

8.62 |

281 |

8.30 |

269 |

8.10 |

279 |

8.14 |

256 |

8.25 |

277 |

8.32 |

271 |

8.50 |

257 |

9.32 |

| |

| The above prices are computed on packer and shipper purchases. |

| RECEIPTS, SHIPMENTS, AND LOCAL SLAUGHTER, WEEK ENDING JULY 29, 1922. |

|---|

| |

| Markets. |

Cattle and calves. |

Hogs. |

Sheep. |

| Receipts. |

Shipments. |

Local slaughter. |

Receipts. |

Shipments. |

Local slaughter. |

Receipts. |

Shipments. |

Local slaughter. |

| Chicago |

61,949 |

14,367 |

47,582 |

141,033 |

30,301 |

110,732 |

69,291 |

19,002 |

50,289 |

| Denver[4] |

6,041 |

4,923 |

1,937 |

6,151 |

60 |

5,885 |

10,743 |

1,958 |

1,698 |

| East St. Louis |

26,146 |

13,103 |

14,721 |

54,947 |

25,404 |

25,941 |

21,991 |

4,597 |

13,814 |

| Fort Worth[4] |

21,089 |

7,681 |

10,727 |

5,472 |

746 |

3,926 |

5,055 |

3,871 |

997 |

| Indianapolis[4] |

8,341 |

4,727 |

4,194 |

44,242 |

15,360 |

28,561 |

4,400 |

1,693 |

2,202 |

| Kansas City |

58,679 |

26,973 |

29,574 |

39,383 |

10,627 |

27,387 |

17,871 |

4,067 |

12,453 |

| Oklahoma City |

10,258 |

5,108 |

4,902 |

7,835 |

695 |

8,028 |

407 |

80 |

295 |

| Omaha |

25,524 |

10,795 |

14,060 |

72,894 |

18,668 |

54,144 |

57,645 |

26,612 |

27,353 |

| St. Joseph[4] |

8,388 |

2,344 |

5,548 |

40,712 |

6,822 |

31,942 |

9,264 |

2,908 |

6,396 |

| St. Paul[4] |

35,933 |

19,472 |

15,369 |

30,560 |

3,616 |

24,224 |

5,982 |

883 |

5,048 |

| Sioux City |

12,746 |

7,336 |

4,314 |

45,910 |

17,483 |

27,478 |

1,060 |

333 |

544 |

| Wichita[4] |

7,415 |

3,739 |

2,614 |

9,915 |

136 |

9,271 |

544 |

|

373 |

| Total |

282,509 |

120,568 |

155,542 |

499,054 |

129,918 |

357,519 |

204,253 |

66,004 |

121,462 |

| Previous week |

298,028 |

106,244 |

182,957 |

443,027 |

112,557 |

330,482 |

239,860 |

52,840 |

172,547 |

108Lamb.—The lamb market showed daily

declines at eastern markets and Chicago

after opening firm to higher on Monday.

Receipts were fairly liberal and demand

poor. Supplies accumulated, although some

lamb was put in the freezers. Compared

with the close of the preceding week, Boston

and New York were $1‒$3 lower, Philadelphia

$2‒$3 lower, and Chicago $1‒$2 lower.

Mutton.—The bulk of the moderate receipts

of mutton at eastern markets was

undesirable because of weight and excessive

finish. Prices were also influenced by the

drop in lamb values, and daily declines were

the rule. At Chicago offerings consisted

largely of heavy ewes and bucks, but prices

showed little change. Compared with the

close of the preceding week, Boston, New

York, and Philadelphia were $2‒$4 lower,

with Chicago unchanged.

Pork.—Fresh light loins were seasonally

scarce and relatively firmer in price than

heavier averages. Receipts of fresh loins

were light, but there was an ample supply

of the frozen product on sale. Compared

with the close of the preceding week, Boston

and Philadelphia were steady to $1 higher

except on heavy loins, which were weak to

$1 lower with some sales off more. New

York closed unevenly $2‒$5 lower, and

Chicago steady to $1 higher.

Wool Imports at Two Ports.

Imports of wool through the port of Philadelphia

during the week ending July 29

amounted to 417,226 lbs., valued at $77,165.

Imports through the port of Boston during

the same week amounted to 2,774,745 lbs.,

having a valuation of $878,563, and in addition

there was received through the port of

Boston 48,776 lbs. of camels’ hair, valued at

$11,986 and 244,767 lbs. of mohair having a

valuation of $56,581.

| CHICAGO WHOLESALE PRICES OF CURED PORK AND PORK PRODUCTS. |

|---|

| |

| [Per 100 pounds.] |

|---|

| |

| |

July 28. |

July 21. |

June 30. |

| Hams, smoked, 14‒16 average |

$26.00‒28.50 |

$27.00‒29.50 |

$28.00‒29.50 |

| Hams, fancy, 14‒16 average |

29.50‒31.50 |

30.00‒32.00 |

31.00‒33.00 |

| Picnics, smoked, 4‒8 average |

17.00‒19.00 |

17.00‒19.00 |

17.00‒19.50 |

| Bacon, breakfast, 6‒8 average |

25.00‒28.00 |

24.00‒28.00 |

25.00‒27.50 |

| Bacon, fancy, 6‒8 average |

32.00‒36.00 |

32.00‒35.50 |

32.00‒35.00 |

| Bellies, D. S., 14‒16 average |

15.50‒16.00 |

15.50‒16.00 |

16.00‒17.00 |

| Backs, D. S., 14‒16 average |

12.00‒13.50 |

12.00‒13.50 |

12.00‒13.00 |

| Pure lard, tierces |

13.00‒14.25 |

12.00‒13.25 |

12.50‒14.00 |

| Compound lard, tierces |

12.75‒14.00 |

12.50‒14.00 |

12.75‒14.00 |

New Zealand’s Production of Butter and Cheese for Export Increases.

The production of butter for export in

New Zealand during the nine months ending

Apr. 30 amounted to 102,637,920 lbs.,

compared with 71,412,650 lbs. during the

corresponding period ending Apr. 30, 1921.

The production of cheese for export during

the nine months ending Apr. 30, was 133,579,600

lbs., compared with 118,628,490 lbs.

for the same period of 1920‒21.

These figures show an increase of 44% in

the production of butter and 12.6% in the

production of cheese. The above figures

relate only to the quantities produced and

graded for export and do not include the

amounts intended for local consumption.

| LIVE STOCK PRICES, TUESDAY, AUGUST 1, 1922. |

|---|

| |

| [Per 100 pounds.] |

|---|

| |

|

|

|

Chicago. |

East St. Louis. |

Kansas City. |

Omaha. |

South St. Joseph. |

St. Paul. |

| CATTLE. |

|

|

|

|

|

|

| Beef steers: |

|

|

|

|

|

|

| |

Medium and heavy (1,101 lbs. up)— |

|

|

|

|

|

|

| |

|

Choice and prime |

$10.00‒10.75 |

$10.00‒10.50 |

$9.85‒10.50 |

$10.00‒10.50 |

$9.75‒10.35 |

|

| |

|

Good |

9.10‒10.00 |

9.25‒10.00 |

8.90‒ 9.85 |

9.25‒10.00 |

8.70‒ 9.75 |

$8.75‒ 9.50 |

| |

|

Medium |

8.15‒ 9.10 |

7.50‒ 9.25 |

7.60‒ 8.90 |

8.00‒ 9.25 |

7.00‒ 8.70 |

7.50‒ 8.75 |

| |

|

Common |

6.65‒ 8.15 |

5.50‒ 7.50 |

6.40‒ 7.60 |

6.00‒ 8.00 |

5.50‒ 7.00 |

5.75‒ 7.50 |

| |

Light weight (1,100 lbs. down)— |

|

|

|

|

|

|

| |

|

Choice and prime |

9.85‒10.65 |

9.75‒10.50 |

9.65‒10.25 |

9.75‒10.50 |

9.65‒10.25 |

|

| |

|

Good |

9.00‒ 9.85 |

9.00‒ 9.75 |

8.65‒ 9.65 |

9.00‒ 9.75 |

8.60‒ 9.65 |

8.75‒ 9.50 |

| |

|

Medium |

8.00‒ 9.00 |

7.50‒ 9.00 |

7.25‒ 8.65 |

7.50‒ 9.00 |

6.85‒ 8.60 |

7.50‒ 8.75 |

| |

|

Common |

6.50‒ 8.00 |

4.75‒ 7.50 |

5.50‒ 7.25 |

5.75‒ 7.50 |

5.25‒ 6.85 |

5.50‒ 7.50 |

| Butcher cattle: |

|

|

|

|

|

|

| |

Heifers, common-choice |

5.15‒ 9.00 |

6.00‒10.00 |

4.75‒ 8.85 |

5.00‒ 9.25 |

5.00‒ 9.00 |

4.00‒ 8.50 |

| |

|

Cows, common-choice |

4.10‒ 8.15 |

4.00‒ 6.25 |

3.85‒ 6.75 |

4.25‒ 7.50 |

3.75‒ 7.50 |

3.75‒ 7.25 |

| |

|

Bulls, bologna and beef |

4.00‒ 6.50 |

3.75‒ 6.25 |

3.50‒ 5.50 |

3.75‒ 6.75 |

3.25‒ 5.75 |

3.25‒ 6.00 |

| Canners and cutters: |

|

|

|

|

|

|

| |

Cows and heifers |

2.85‒ 4.10 |

2.50‒ 4.00 |

2.35‒ 3.85 |

2.75‒ 4.25 |

2.25‒ 3.75 |

2.25‒ 3.75 |

| |

Canner steers |

3.50‒ 5.25 |

3.25‒ 4.00 |

3.00‒ 4.25 |

3.00‒ 4.25 |

|

2.75‒ 4.00 |

| Veal calves: |

|

|

|

|

|

|

| |

Light and med. wt., med.-choice |

9.00‒10.50 |

6.50‒10.00 |

6.25‒ 9.25 |

7.50‒ 9.50 |

6.25‒ 9.25 |

4.00‒ 9.00 |

| |

Heavy weight, common-choice |

4.00‒ 8.00 |

3.50‒ 7.50 |

4.00‒ 8.25 |

5.25‒ 7.75 |

5.00‒ 7.00 |

3.59‒ 7.00 |

| Feeder steers: |

|

|

|

|

|

|

| |

1,001 lbs. up, common-choice |

5.50‒ 7.65 |

5.75‒ 7.50 |

6.15‒ 8.40 |

5.75‒ 8.25 |

5.25‒ 8.00 |

4.25‒ 7.25 |

| |

750‒1,000 lbs., common-choice |

5.50‒ 7.65 |

4.75‒ 7.50 |

6.10‒ 8.35 |

5.25‒ 8.00 |

5.25‒ 8.00 |

3.75‒ 7.25 |

| Stocker cattle: |

|

|

|

|

|

|

| |

Steers, common-choice |

4.75‒ 7.65 |

3.50‒ 7.50 |

4.60‒ 8.10 |

5.00‒ 7.75 |

4.50‒ 7.50 |

3.50‒ 7.00 |

| |

Cows and heifers, common-choice |

3.50‒ 5.75 |

3.00‒ 5.50 |

3.25‒ 5.85 |

3.50‒ 5.75 |

3.25‒ 5.50 |

2.75‒ 5.50 |

| |

Calves— |

|

|

|

|

|

|

| |

|

Good and choice |

|

|

6.75‒ 7.75 |

7.00‒ 8.00 |

|

|

| |

|

Common and medium |

|

|

4.00‒ 6.50 |

5.00‒ 7.00 |

|

|

| HOGS. |

|

|

|

|

|

|

| Top |

10.75 |

10.75 |

10.20 |

10.30 |

10.10 |

10.25 |

| Bulk of sales |

8.10‒10.65 |

10.25‒10.65 |

9.00‒10.10 |

7.75‒10.25 |

9.50‒10.10 |

7.50‒10.00 |

| Heavy wt. (251 lbs. up), common-choice |

9.80‒10.30 |

9.25‒10.25 |

9.00‒ 9.75 |

9.00‒10.00 |

9.00‒9.90 |

8.25‒10.00 |

| Med. wt. (201‒250 lbs.), common-choice |

10.20‒10.65 |

10.15‒10.70 |

9.75‒10.05 |

9.65‒10.25 |

9.85‒10.10 |

8.75‒10.00 |

| Light wt. (151‒200 lbs.), common-choice |

10.50‒10.70 |

10.60‒10.75 |

9.70‒10.20 |

10.00‒10.25 |

9.90‒10.10 |

9.75‒10.25 |

| Light lts. (131‒150 lbs.), common-choice |

10.25‒10.65 |

10.50‒10.75 |

9.60‒10.10 |

|

|

|

| Packing sows (250 lbs. up), smooth |

8.00‒ 8.65 |

7.75‒ 8.00 |

7.50‒ 7.85 |

7.75‒ 8.50 |

7.65‒ 8.00 |

7.25‒ 8.25 |

| Packing sows (200 lbs. up), rough |

7.25‒ 8.00 |

7.60‒ 7.75 |

7.25‒ 7.50 |

7.25‒ 7.75 |

7.25‒ 7.60 |

6.75‒ 7.25 |

| Pigs (150 lbs. down), common-choice |

9.75‒10.40 |

10.00‒10.60 |

|

|

|

|

| Stock pigs (130 lbs. down) |

|

9.75‒10.25 |

9.75‒10.50 |

9.00‒10.00 |

|

10.00‒10.50 |

| SHEEP. |

|

|

|

|

|

|

| Lambs: |

|

|

|

|

|

|

| |

84 lbs. down, medium-choice |

11.50‒12.75 |

11.00‒12.25 |

10.25‒13.00 |

11.50‒12.25 |

11.50‒13.00 |

11.00‒12.25 |

| |

Culls and common |

7.50‒11.25 |

5.50‒11.00 |

6.00‒10.00 |

7.25‒11.50 |

7.00‒11.25 |

|

| |

Feeding lambs |

11.50‒12.50 |

|

|

9.25‒12.00 |

|

|

| Yearlings, wethers, medium-prime |

8.50‒11.00 |

8.00‒10.75 |

7.00‒10.50 |

8.25‒10.50 |

7.50‒11.00 |

6.50‒10.50 |

| Wethers, medium-prime |

6.00‒ 8.75 |

5.50‒ 8.25 |

6.25‒ 8.25 |

6.25‒ 8.75 |

6.00‒ 8.00 |

7.50‒10.25 |

| Ewes: |

|

|

|

|

|

|

| |

Medium, good, and choice |

3.25‒ 7.60 |

3.00‒ 6.00 |

5.00‒ 7.00 |

4.00‒ 7.00 |

4.00‒ 7.00 |

4.00‒ 8.25 |

| |

Culls and common |

2.00‒ 3.75 |

1.50‒ 3.00 |

2.00‒ 5.00 |

2.00‒ 4.00 |

1.50‒ 4.00 |

3.00‒ 6.75 |

| |

Breeding ewes (full mouths to yearlings) |

5.00‒11.50 |

5.50‒ 8.50 |

5.75‒ 9.00 |

|

|

2.00‒ 3.50 |

| WHOLESALE PRICES OF WESTERN DRESSED MEATS, TUESDAY, AUGUST 1, 1922. |

|---|

| |

| [Per 100 pounds.] |

|---|

| |

|

|

|

Chicago. |

New York. |

|

|

|

Aug. 1. |

July 25. |

July 3. |

Aug. 1. |

July 25. |

July 3. |

| Fresh beef: |

|

|

|

|

|

|

| |

Steers— |

|

|

|

|

|

|

| |

|

Choice |

$15.50‒16.00 |

$16.50‒17.00 |

$15.00‒16.00 |

$16.50‒17.00 |

$16.00‒17.00 |

$17.00‒17.50 |

| |

|

Good |

14.50‒15.00 |

15.50‒16.00 |

14.50‒15.00 |

14.00‒16.00 |

15.50‒16.00 |

16.00‒17.00 |

| |

|

Medium |

13.00‒14.00 |

14.00‒15.00 |

13.00‒14.00 |

11.00‒13.00 |

13.00‒15.00 |

15.00‒16.00 |

| |

|

Common |

10.00‒12.00 |

11.00‒13.00 |

12.00‒13.00 |

8.00‒10.00 |

10.00‒12.50 |

12.00‒15.00 |

| |

Cows— |

|

|

|

|

|

|

| |

|

Good |

11.50‒12.50 |

12.00‒13.00 |

12.00‒12.50 |

11.00‒12.00 |

13.00 |

13.00‒14.00 |

| |

|

Medium |

10.50‒11.50 |

11.00‒12.00 |

11.00‒11.50 |

9.00‒11.00 |

11.00‒12.50 |

12.00‒13.00 |

| |

|

Common |

8.50‒ 9.50 |

9.00‒10.00 |

9.00‒10.00 |

8.00‒ 9.00 |

10.00‒11.00 |

11.00‒12.00 |

| |

Bulls— |

|

|

|

|

|

|

| |

|

Good |

|

|

|

10.00 |

11.00 |

12.00‒12.50 |

| |

|

Medium |

|

|

|

9.00‒10.00 |

9.00‒10.50 |

10.00‒12.00 |

| |

|

Common |

7.50‒ 7.75 |

7.75‒ 8.25 |

7.00‒ 7.25 |

7.00‒ 8.00 |

8.00‒ 9.00 |

9.00‒10.00 |

| Fresh veal: |

|

|

|

|

|

|

| |

Choice |

16.00‒17.00 |

16.00‒17.00 |

15.00‒17.00 |

16.00‒18.00 |

17.00‒18.00 |

15.00‒16.00 |

| |

Good |

14.00‒15.00 |

15.00‒16.00 |

14.00‒15.00 |

13.00‒15.00 |

15.00‒17.00 |

12.00‒14.00 |

| |

Medium |

12.00‒13.00 |

12.00‒14.00 |

13.00‒14.00 |

11.00‒12.00 |

12.00‒15.00 |

10.00‒12.00 |

| |

Common |

10.00‒11.00 |

10.00‒11.00 |

8.00‒12.00 |

10.00‒11.00 |

9.00‒11.00 |

8.00‒10.00 |

| Fresh pork cuts: |

|

|

|

|

|

|

| |

Loins— |

|

|

|

|

|

|

| |

|

8‒10 lbs. average |

23.00‒25.00 |

23.00‒24.00 |

22.00‒23.00 |

23.00‒24.00 |

23.00‒24.00 |

22.00‒23.00 |

| |

|

10‒12 lbs. average |

20.00‒22.00 |

20.00‒22.00 |

21.00‒22.00 |

22.00‒23.00 |

22.00‒23.00 |

21.00‒22.00 |

| |

|

12‒14 lbs. average |

17.00‒19.00 |

17.00‒19.00 |

19.00‒20.00 |

21.00‒22.00 |

21.00‒22.00 |

20.00‒21.00 |

| |

|

14‒16 lbs. average |

14.00‒16.00 |

15.00‒16.00 |

18.00‒19.00 |

18.00‒20.00 |

20.00‒21.00 |

19.00‒20.00 |

| |

|

16 lbs. and over |

12.00‒14.00 |

13.00‒14.00 |

16.00‒18.00 |

16.00‒18.00 |

18.00‒20.00 |

18.00‒19.00 |

| |

Shoulders— |

|

|

|

|

|

|

| |

|

Skinned |

13.50‒14.50 |

13.50‒14.50 |

14.00‒15.00 |

15.00‒16.00 |

15.00‒16.00 |

15.00‒16.00 |

| |

Picnics— |

|

|

|

|

|

|

| |

|

4‒6 lbs. average |

14.00‒15.00 |

15.00‒16.00 |

15.00‒15.50 |

|

|

|

| |

|

6‒8 lbs. average |

13.00‒14.00 |

14.00‒15.00 |

14.50‒15.00 |

15.00‒16.00 |

14.00‒16.00 |

16.00‒17.00 |

| |

Butts— |

|

|

|

|

|

|

| |

|

Boston style |

16.00‒17.50 |

16.00‒17.50 |

16.00‒17.00 |

18.00‒19.00 |

16.00‒18.00 |

17.00‒19.00 |

| Fresh lamb and mutton: |

|

|

|

|

|

|

| |

Lamb— |

|

|

|

|

|

|

| |

|

Choice |

26.00‒27.00 |

27.00‒28.00 |

26.00‒28.00 |

25.00‒20.00 |

26.00‒21.00 |

24.00‒27.00 |

| |

|

Good |

24.00‒25.00 |

26.00‒27.00 |

24.00‒26.00 |

22.00‒23.00 |

24.00‒25.00 |

18.00‒20.00 |

| |

|

Medium |

21.00‒23.00 |

23.00‒25.00 |

21.00‒23.00 |

21.00‒22.00 |

22.00‒23.00 |

16.00‒18.00 |

| |

|

Common |

16.00‒20.00 |

16.00‒21.00 |

15.00‒20.00 |

19.00‒21.00 |

16.00‒20.00 |

12.00‒14.00 |

| |

Mutton— |

|

|

|

|

|

|

| |

|

Good |

14.00‒15.00 |

14.00‒15.00 |

13.00‒14.50 |

13.00‒16.00 |

15.00‒17.00 |

14.00‒16.00 |

| |

|

Medium |

10.00‒12.00 |

10.00‒12.00 |

10.00‒12.00 |

10.00‒12.50 |

13.00‒14.00 |

10.00‒12.00 |

| |

|

Common |

6.00‒ 8.00 |

6.00‒ 8.00 |

6.00‒ 8.00 |

7.00‒10.00 |

10.00‒13.00 |

8.00‒10.00 |

109

WEEKLY LIVE STOCK REVIEW.

(Concluded from page 107.)

were considerably heavier. Chicago quality

was the best for several weeks, a generous

proportion of the supply consisting of good

light and medium weight butchers. This,

coupled with the narrowest shipping outlet

for hogs in weeks, attributed to an extent to

unsettled railway labor conditions, was partially

responsible for sharp declines, especially

on the better grades. Closing prices

Were 40¢‒55¢ under those of the week previous

on bulk of good lights and butchers

and 25¢‒50¢ lower on mixed and packing

grades. A slight reaction was noticed toward

the week end, with small advances

scored on some of the in-between butchers

and better packing grades.

Big packers were bearish and very indifferent

buyers, even at the sharp decline,

leaving liberal holdovers each day. The

week’s top at Chicago was $11, secured on

early sessions for good lights and light

butchers, but best sold at the close at $10.60,

and bulk of good lights and light butchers

sold at the week end from $10.30‒$10.50.

Bulk of good 220 lb.‒300 lb. butchers closed

at $9.75‒$10.25. Such shipping orders as

were filled called largely for the better

grades of mixed packing, good, smooth,

light weight sows and these failed to show

the extreme decline apparent on other

grades.

GOOD PIGS IN DEMAND.

Demand for good pigs at Chicago was

broad and such sold readily all week, with

bulk of good 100‒130 lb. averages clearing

from $9.50‒$10.50. Saturday’s closing

values on pigs were around 25¢ lower for

the week. Stock pig prices, both at St.

Paul and Missouri River markets declined

25¢‒35¢, best strong weights selling at

$10.25‒$10.50 at St. Paul and Kansas City,

respectively. Several shipments of good

quality thin sows went to the country from

St. Paul and Chicago for feeding purposes,

costing $8‒$9. The trade generally displayed

considerable anxiety on account of

the railway and coal strikes.

Sheep.—An oversupply of sheep at Jersey

City at the week’s opening was the chief

factor in further declines in prices following

the declines late last week at Chicago and

other western markets, but with aggregate

slaughter falling considerably short of the

week previous, the market made good

recovery as the week’s trading progressed.

Closing Chicago prices, compared with the

week previous, were strong to 25¢ higher

on fat native lambs, mostly 50¢ higher on

cull natives, steady to 15¢ lower on fat

western lambs, 35¢‒50¢ lower on western

feeding lambs, generally steady on light

sheep and 25¢‒50¢ lower on heavy sheep.

Subsequent to Monday when Jersey City

had a full supply, the run of southeastern

lambs was light and natives from other

sections were in smaller supply than during

the preceding week. The market-ward

movement of range stock from the Northwest

was of fair volume, although hampered

to a certain extent by conditions

arising from the strike of railway shopmen.

Feeder demand was narrow at the week’s

opening but declines then enforced attracted

buyers subsequently and both fat

and feeder lambs closed about 25¢ above

the week’s low spot.

At the week end, choice western lambs

were safely quotable up to $13 at Chicago,

good Oregons, rather lightly sorted, selling

up to $12.85, and best natives up to $12.75

straight, with bulk of natives at $12.50$12.60

and native culls mostly at $8‒$8.50.

Feeder buyers paid up to $12.50 for light and

tidy weight Western feeder lambs, but a

number of loads of heavy feeders sold during

the week at $11.50‒$11.75. Fat heavy ewes

sold downward to $3, a few below $3.50 at

the close, while fat light native and Western

ewes reached $7‒$7.25. Wethers and yearlings

were virtually lacking. There was call

for western yearling breeding ewes, with

none offered and choice quotable to $11.50.

Native yearling ewes were taken on breeder

account up to $9.50‒$9.75, twos to fours

mixed up to $8‒$8.75, with heavies and less

desirable kinds on down to $6 and below,

depending on age, weight, and quality.

Opening, July 31.—Beef steers, yearlings,

butcher cows, and heifers at Chicago sold

actively at strong to 25¢ higher prices,

mostly 10¢‒15¢ higher. Eleven loads of

matured beef steers averaging 1,283 lbs.‒1,694

lbs. topped at $10.60. Best long yearlings

brought $10.50, bulk of beef steers $8.50‒$10.15.

Twelve loads of Canadian steers

arrived, five loads going to stocker and feeder

dealers at $5.75. Stockers and feeders displayed

some strength.

Good butcher weight hogs gained 10¢‒15¢

and closed firm at the advance. Top was

$10.70 with bulk of desirable butchers at

$9.90‒$10.60. Activity of shippers, who absorbed

around 10,000 head, lent zest and

higher prices to the better grades. Mixed

and packing grades opened higher, but

lacking good competition closed steady to

150 lower, bulk of packing sows turning at

$7.75‒$8.60.

Fat lambs closed weak to 15¢ lower after a

steady to strong start. Natives and westerns

topped at $12.75, bulk of the natives bringing

$12.25‒$12.60 and bulk of the rangers

$12.65. Feeding lambs at $12.35 downward

were lower. Sheep held firm. Choice handy

Montana ewes reached $7.50.

| STOCKER AND FEEDER SHIPMENTS. |

|---|

| |

| Week Ending Friday, July 28, 1922. |

|---|

| |

|

|

Cattle and calves. |

Hogs. |

Sheep. |

| Market origin: |

|

|

|

| |

Chicago |

4,077 |

|

17,432 |

| |

Denver |

4,368 |

286 |

241 |

| |

East St. Louis |

3,317 |

836 |

492 |

| |

Fort Worth |

1,406 |

170 |

1,369 |

| |

Indianapolis |

908 |

192 |

772 |

| |

Kansas City |

18,483 |

917 |

1,919 |

| |

Oklahoma City |

2,996 |

120 |

|

| |

Omaha |

8,591 |

75 |

19,861 |

| |

St. Joseph |

2,098 |

298 |

2,798 |

| |

St. Paul |

13,441 |

1,169 |

883 |

| |

Sioux City |

5,786 |

353 |

333 |

| |

Wichita |

1,512 |

136 |

|

| Total |

66,983 |

4,552 |

46,100 |

| |

Previous week |

47,627 |

5,140 |

34,919 |

| |

Same week last year[5] |

28,747 |

2,161 |

41,592 |

| State destination: |

|

|

|

| |

California |

|

170 |

|

| |

Colorado |

1,374 |

286 |

|

| |

Illinois |

8,458 |

826 |

3,681 |

| |

Indiana |

2,105 |

192 |

3,521 |

| |

Iowa |

17,302 |

1,266 |

8,695 |

| |

Kansas |

6,716 |

266 |

1,380 |

| |

Kentucky |

487 |

366 |

1,202 |

| |

Maryland |

101 |

|

310 |

| |

Michigan |

308 |

|

11,445 |

| |

Minnesota |

1,014 |

397 |

513 |

| |

Missouri |

5,654 |

588 |

4,159 |

| |

Montana |

493 |

|

|

| |

Nebraska |

14,942 |

75 |

9,417 |

| |

New York |

48 |

|

|

| |

Ohio |

1,009 |

|

801 |

| |

Oklahoma |

735 |

120 |

|

| |

Pennsylvania |

3,894 |

|

|

| |

South Dakota |

837 |

|

|

| |

Tennessee |

36 |

|

|

| |

Texas |

901 |

|

270 |

| |

Virginia |

129 |

|

411 |

| |

West Virginia |

59 |

|

121 |

| |

Wisconsin |

323 |

|

174 |

| |

Wyoming |

58 |

|

|

| Total |

66,983 |

4,552 |

46,100 |

New Publications Issued.

The following publications were issued by

the U. S. Department of Agriculture during

the week ending Aug. 1, 1922. A copy of

any of them, except those otherwise noted,

may be obtained free upon application to

the Chief of the Division of Publications,

U. S. Department of Agriculture, as long

as the department’s supply lasts.

After the department’s supply is exhausted,

publications can be purchased

from the Superintendent of Documents,

Government Printing Office, Washington,

D. C. Purchase order and remittance

should be addressed to the Superintendent

of Documents direct and not to the Department

of Agriculture.

Sugar Beet Growing Under Irrigation. By C. O.

Townsend, Pathologist in Charge of Sugar-Plant

Investigations. Pp. 32, figs. 17. Contribution

from the Bureau of Plant Industry. Revised June,

1922. (Farmers’ Bulletin 567.)

The Insulating Value of Commercial Double-Walled

Beehives. By E. F. Phillips, Apiculturist in Charge,

Bee-Culture Investigations. Pp. 9. Contribution

from the Bureau of Entomology. May, 1922. (Department

Circular 222.) Price, 5¢.

A Handbook of Dairy Statistics. By T. R. Pirtle, Dairy

Division. Pp. 72, fig. 1. Contribution from the

Bureau of Animal Industry. June, 1922. (A. I. 37.)

Price, 15¢.

Vegetable Growing in Guam. By Glen Briggs, Agronomist

and Horticulturist. Pp. 60, pls. 17. June,

1922. (Bulletin 2, Guam Agricultural Experiment

Station.)

| COLD STORAGE HOLDINGS OF FROZEN AND CURED FISH, JULY 15, 1922. |

|---|

| |

| [Thousands of pounds; i. e., 000 omitted.] |

|---|

| |

| Species. |

Total holdings June 15, 1921. |

Total holdings July 15, 1921. |

Total holdings June 15, 1922. |

Frozen since June 15, 1922. |

Total holdings July 15, 1922.[6] |

| FROZEN FISH. |

|

|

|

|

|

| Bluefish |

128 |

114 |

65 |

97 |

147 |

| Butterfish |

153 |

154 |

46 |

83 |

139 |

| Catfish |

[7] |

[7] |

[7] |

33 |

93 |

| Ciscoes |

2,525 |

2,605 |

1,080 |

167 |

987 |

| Ciscoes (tullibees) |

[8] |

[8] |

1,136 |

2 |

1,068 |

| Cod, haddock, hake, pollack |

1,955 |

1,916 |

391 |

26 |

339 |

| Croakers |

187 |

277 |

24 |

65 |

75 |

| Flounders |

[7] |

[7] |

[7] |

23 |

233 |

| Halibut |

4,375 |

6,213 |

3,878 |

742 |

4,380 |

| Herring, sea |

2,889 |

3,775 |

1,121 |

127 |

1,085 |

| Lake trout |

944 |

1,032 |

498 |

109 |

562 |

| Mackerel |

1,695 |

1,670 |

1,929 |

624 |

2,422 |

| Pike perches and pike or pickerel |

[7] |

[7] |

[7] |

28 |

294 |

| Sablefish |

270 |

456 |

580 |

56 |

492 |

| Salmon, silver and fall |

658 |

905 |

344 |

346 |

656 |

| Salmon, steelhead trout |

[9] |

[9] |

118 |

103 |

209 |

| Salmon, all other |

963 |

2,182 |

719 |

785 |

1,138 |

| Scup (porgies) |

[7] |

[7] |

[7] |

913 |

1,043 |

| Shad and shad roe |

250 |

324 |

273 |

22 |

299 |

| Shellfish |

[7] |

[7] |

[7] |

32 |

235 |

| Smelts, eulachon, etc. |

248 |

268 |

351 |

1 |

333 |

| Squeteagues, or “seatrout” |

263 |

1,405 |

283 |

40 |

260 |

| Squid |

3,026 |

3,170 |

1,036 |

92 |

1,039 |

| Sturgeon or spoonbill cat |

[7] |

[7] |

[7] |

88 |

257 |

| Suckers |

[7] |

[7] |

[7] |

|

16 |

| Whitefish |

985 |

1,278 |

1,427 |

50 |

1,439 |

| Whiting |

2,690 |

4,499 |

1,445 |

1,857 |

3,048 |

| Miscellaneous |

8,107 |

7,917 |

4,074 |

865 |

3,313 |

| Total |

32,311 |

40,160 |

20,818 |

7,376 |

25,601 |

| |

|

|

|

|

|

| CURED FISH. |

|

|

|

|

|

| Herring |

9,210 |

8,389 |

12,991 |

|

13,425 |

| Mild cured salmon |

1,672 |

3,140 |

2,358 |

|

3,849 |

110

Dairy and Poultry

BUTTER MARKETS DROP UNDER ACCUMULATIONS OF RECEIPTS

Prices Fluctuate During Week—Large Increase in Consumption Over 1921 So Far This Year.

Increasing accumulations of butter and

lack of confidence among members of the

trade were the principal factors in bringing

about extremely weak conditions and

radical declines in all markets during the

early part of the week ending July 29. The

resulting lower prices attracted a speculative

demand which was largely instrumental in

causing equally radical advances during the

latter part of the week. The prices at the

close of the week, however, hovered near

the same levels as at the opening, and conditions,

although not so extremely weak

because of lighter stocks, were equally unsettled.

Since early in July receivers have been

burdened with heavy accumulations of

receipts because of the curtailed storing

demand, and the strength of the market has

been maintained by the hope that consuming

outlets would become larger, that

receipts would decrease more rapidly, or

that exporters would take considerable

quantities. When there appeared to be no

immediate outlet for the accumulating

stocks, dealers slashed prices and cleared

away a large part of the accumulations.

SPECULATIVE INTEREST DEVELOPS.

The lower prices, however, brought forth

a speculative interest which was so keen

that prices reacted practically to the level

on Monday. But with the higher prices

buyers again disappeared, the market became

very unsettled, and some price reductions

ensued.

The strengthening factors are an excellent

consumptive demand, possibilities of export

and the improbability of any considerable

imports. A shortage in stocks of butter in

foreign markets makes it probable that considerable

butter will be exported and improbable

that the imports will be large. Aside

from the possibility of exports and imports,

the enormous quantity of butter going into

consumption is a major factor in the possible

trend of the markets.

Receipts at the four markets since Jan. 1

show a surplus of some 58,000,000 lbs. over

the same period a year ago. Of these

receipts, nearly 11,000,000 lbs. in excess of

last year was stored. Import and export

figures for the first six months of the year

show an excess of exports over imports of

2,365,000 lbs. During the corresponding

period in 1921 there was an excess of imports

amounting to 6,139,000 lbs. Deducting the

11,000,000 lbs. which was stored in excess of

last year and the decrease of 8,000,000 lbs.

due to foreign trade, the apparent increase

in consumption since Jan. 1, 1922, amounts

to some 39,000,000 lbs.

On the other hand, while larger quantities

have gone into consumption there are

some operators who are bearish and claim

that prices will have to rule higher next

winter than last winter in order to allow a

fair profit on present storage stocks, and that

this condition naturally would reduce consumption.

It is claimed also that production

may continue comparatively heavy,

making large outlets necessary. Some also

point out that during our winter months the

countries in the Southern Hemisphere have

their season of flush production and that

imports from those countries are a possibility.

Notwithstanding the fact that the markets

at present are weak and unsettled, and

receivers generally desire to keep current

receipts moving, most of those owning storage

butter have confidence in holding it at

its present cost.

| WHOLESALE PRICES OF BUTTER AND CHEESE, WEEK ENDING JULY 29, 1922. |

|---|

| |

| [Cents per pound.] |

|---|

| |

| CREAMERY BUTTER (92 score). |

New York. |

Chicago. |

Philadelphia. |

Boston. |

San Francisco. |

| Monday |

35 |

33 |

36 |

36 |

37¼ |

| Tuesday |

34 |

32½ |

35 |

35½ |

37 |

| Wednesday |

34½ |

32½ |

35 |

35½ |

37 |

| Thursday |

35½ |

34 |

36 |

36 |

37¼ |

| Friday |

34½ |

33½ |

35½ |

35½ |

37 |

| Saturday |

34 |

33½ |

35½ |

35½ |

37 |

| Average for week |

34.68 |

33.17 |

35.50 |

35.67 |

37.08 |

| Previous week |

36.08 |

34.08 |

36.67 |

36.67 |

39.37 |

| Corresponding week last year |

42.67 |

41.42 |

43.08 |

43.50 |

39.62 |

| AMERICAN CHEESE (No. 1 fresh twins) |

New York. |

Chicago. |

Boston. |

San Francisco.[10] |

Wisconsin. |

| Monday |

20½‒21¼ |

18½‒19 |

21½‒22½ |

19¼ |

18¼ |

| Tuesday |

20¼‒21 |

18½‒19 |

21½‒22¼ |

19¼ |

18½ |

| Wednesday |

20¼‒21 |

18½‒19 |

21½‒22¼ |

20 |

18½ |

| Thursday |

20¼‒21 |

18½‒19 |

21½‒22 |

19¾ |

18¼ |

| Friday |

20¼‒21 |

18½‒19 |

21½‒22 |

19¾ |

18 |

| Saturday |

20¼‒21 |

18½‒19 |

21 ‒21½ |

19¾ |

18 |

| Average for week |

20.67 |

18.75 |

21.68 |

19.62 |

18.26 |

| Previous week |

21.13 |

18.83 |

22.00 |

19.21 |

18.71 |

| Corresponding week last year |

21.00 |

20.44 |

21.42 |

22.08 |

21.04 |

| Wholesale Prices of Centralized Butter (90 score) at Chicago. |

|---|

| |

| [Cents per pound.] |

|---|

| |

| Monday |

32¼ |

| Tuesday |

31¾ |

| Wednesday |

32¼ |

| Thursday |

33 |

| Friday |

32¾ |

| Saturday |

32¾ |

| |

|

| Average |

32.46 |

| MOVEMENT AT FIVE MARKETS. |

|---|

| |

| [New York, Chicago, Philadelphia, Boston, and San Francisco.] |

|---|

| |

|

Week ending July 29. |

Previous week. |

Last year. |

| BUTTER. |

Pounds. |

Pounds. |

Pounds. |

| Receipts for week |

16,406,388 |

17,848,858 |

13,737,695 |

| Receipts since Jan. 1 |

406,421,998 |

390,015,610 |

333,511,550 |

| Put into cold storage |

5,763,120 |

6,227,574 |

4,363,777 |

| Withdrawn from cold storage |

1,196,527 |

1,090,911 |

2,391,506 |

| Change during week |

+4,566,593 |

+5,136,663 |

+1,972,271 |

| Total holdings |

58,529,169 |

53,962,576 |

49,378,903 |

| CHEESE. |

|

|

|

| Receipts for week |

4,760,350 |

4,368,795 |

4,034,423 |

| Receipts since Jan. 1 |

113,423,195 |

108,662,845 |

109,844,370 |

| Put into cold storage |

2,212,808 |

2,824,638 |

2,780,994 |

| Withdrawn from cold storage |

1,297,907 |

1,185,107 |

1,753,219 |

| Change during week |

+914,901 |

+1,639,531 |

+1,027,775 |

| Total holdings |

17,542,277 |

16,627,376 |

15,250,616 |

| DRESSED POULTRY. |

|

|

|

| Receipts for week |

3,039,791 |

3,237,754 |

2,455,183 |

| Receipts since Jan. 1 |

107,262,094 |

104,222,303 |

91,359,363 |

| Put into cold storage |

1,039,930 |

1,211,646 |

745,099 |

| Withdrawn from cold storage |

2,114,313 |

2,144,566 |

1,518,844 |

| Change during week |

‒1,074,383 |

‒932,920 |

‒773,745 |

| Total holdings |

23,316,211 |

24,390,594 |

15,513,172 |

| EGGS. |

Cases. |

Cases. |

Cases. |

| Receipts for week |

273,535 |

293,498 |

236,614 |

| Receipts since Jan. 1 |

12,471,456 |

12,197,921 |

11,265,592 |

| Put into cold storage |

76,188 |

74,222 |

45,631 |

| Withdrawn from cold storage |

34,863 |

29,352 |

70,151 |

| Change during week |

+41,325 |

+44,870 |

‒24,520 |

| Total holdings |

4,995,153 |

4,953,828 |

3,645,439 |

CHEESE PRICES LOWER UNDER LIGHT CONSUMPTIVE DEMAND

Speculative Demand Also Lacking—Prices Down a Full Cent at Wisconsin Primary Markets.

The light summer consumptive demand

without the support of speculative storage

activity has been insufficient to clear the

current make of cheese during the past few

weeks, and as a consequence a weaker feeling

developed. During the week ending July

29 this weakness became more pronounced,

and prices at the Wisconsin primary markets

were lowered as much as a full cent in an

effort to stimulate trading.

Buyers, however, were not eager to take

on any more goods than could be readily

used to meet daily requirements. Although

a few cars of fine cheese were purchased

early in the week for storage, the majority

of buyers felt that the market was on too

high a plane for speculation.

SPECULATIVE DEMAND ABSENT.

The absence of speculative support has

probably been the largest factor in the

weaker country markets, and the reflection

of this weakness in the distributing markets.

Moreover, movement into consumptive

channels has not been active for some time.

As storage demand has been lacking and the

primary markets have been showing signs

of weakening, most buyers at distributing

points adopted the policy of hand-to-mouth

buying in anticipation of lower prices.

Advices at the end of the week indicated

that some dealers do not look for a revival of

trade until prices at country points reach

16¢, about 2¢ below present prices. However,

this sentiment is not universal, and

many dealers think that present prices may

not be far from bottom.

Embargoes on railroad shipments of perishable

foodstuffs in the southern and southwestern

sections of the country have reduced

shipments below normal requirements, and

until the rail strike is ended but little support

is expected from those sections. In

fact, many in the trade believe that while

the strike may cause higher prices in certain

consuming centers where supplies are

exhausted, embargoes on shipments will

tend to weaken the primary markets because

of curtailed outlets.

At the close of the week the tone of the

market was barely steady. Holders were

free sellers, and in many instances were inclined

to make concessions in order to keep

stocks as low as possible. Little export or

import business was reported, although

small shipments of Split Twins were imported

from Canada. However, both the

export and import business was of small

consequence and did not affect the market.

With production in excess of consumption

and speculators off the market, many in the

trade expect an unsettled market accompanied

by lower prices.

| IMPORTS OF EGGS DURING JUNE, 1922. |

|---|

| |

| [Data from the Department of Commerce.] |

|---|

| |

| Imported from— |

Eggs in the shell |

Dried and frozen eggs. |

Egg albumen. |

| |

Dozen. |

Pounds. |

Pounds. |

| Denmark |

2,100 |

|

|

| Canada |

16,957 |

12,800 |

|

| China |

72 |

865,000 |

374,140 |

| Hongkong |

24,319 |

7,636 |

300 |

| Other countries |

6 |

|

|

| Total: |

|

|

|

| June, 1922 |

43,454 |

885,436 |

374,440 |

| June, 1921 |

44,941 |

726,596 |

293,948 |

| Jan. to June, 1922 |

632,189 |

4,840,377 |

4,072,171 |

| Jan. to June, 1921 |

2,471,167 |

6,198,562 |

1,322,519 |

111

CONDENSED AND EVAPORATED MILK MARKETS STILL SLOW

Domestic Products Meeting With More Competition From European Goods—Exports Decrease.

The same relative inactivity which has

featured condensed and evaporated milk

markets for several months continued during

July, and prospects for any materially

improved demand are so slight that many of

the trade who have held a more or less confident

attitude are beginning to lose some of

their optimism.

Export demand, upon which canned

milk manufacturers have come to depend to

a large extent as an outlet for surplus domestic

production, has become less of a factor

each month. Buying for relief purposes,

which constituted such a support to the

evaporated milk market especially, has

practically ceased, and no additional orders

seem to be in sight.

LITTLE FOREIGN DEMAND EXPECTED.

Domestic demand in England is reported

as somewhat heavier, but American manufacturers

have as competitors an increasing

number of European factories which are able

to lay down the goods at a lower cost. In

fact, foreign demand is not expected to absorb

very large quantities of American-made

goods in the very near future. Latest export

figures are for the month of June and

indicate a slight decrease under May and a

very large decrease under June, 1921.

Condenseries, however, have had at least

one favorable condition during the past few

months which has helped considerably to

offset the dull demand for canned milk.

Prices of both butter and cheese have been

at levels that made it possible to divert surplus

milk into one or the other of these

products, and as a result the production of

condensed and evaporated goods has been

held as low as was consistent with good

business practice. These outlets have been

fortunate not only because of the lighter

demand which has featured both condensed

and evaporated milk markets, but because

of the upward tendency of costs of manufacturing

as well. Seasonal advances in

prices of raw milk are almost at hand, and

in the case of condensed milk, sugar is over

one-third higher in cost than it was in the